Form 990 Heading

An item-by-item review of the core identifying information required in the Form 990 heading

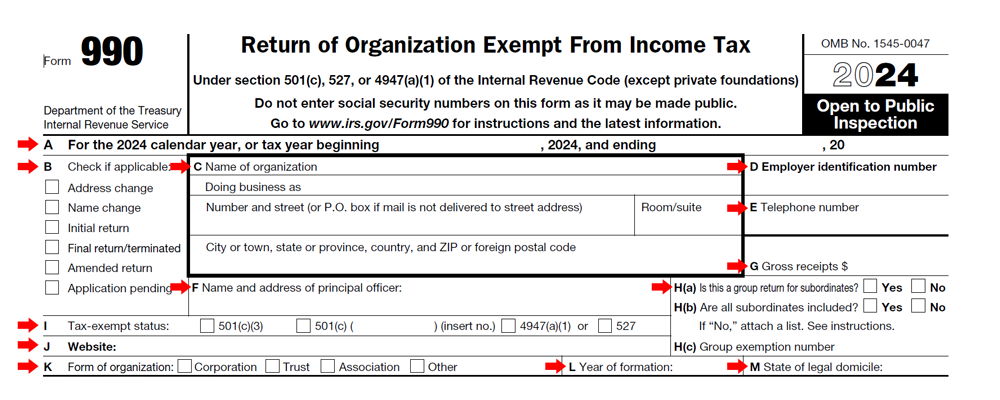

📌 The heading of Form 990 provides the IRS and the public with a snapshot of the filing organization’s core identity. This section captures essential details, including the organization’s legal name, address, and Employer Identification Number (EIN), as well as its form of organization, tax-exempt status, and the specific fiscal year covered by the return.

| Item | Question | Item Instructions | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| A | For the [Form Year] calendar year, or tax year beginning __________, [Form Year], and ending __________, [Form Year + 1] | Item A. Accounting period. An organization must file the version of the Form 990 that corresponds to the year in which its accounting period begins.

|

||||||||

| B | Check if applicable:

| Item B. Checkboxes. The following checkboxes are under item B. Address change. Check this box if the organization changed its address and hasn’t reported the change on its most recently filed Form 990; 990-EZ; 990-N; or 8822-B, Change of Address or Responsible Party—Business, or in correspondence to the IRS. TIP: If a change in address occurs after the return is filed, use Form 8822-B to notify the IRS of the new address. Name change.Check this box if the organization changed its legal name (not its “doing business as” name) and if the organization hasn’t reported the change on its most recently filed Form 990 or 990-EZ or in correspondence to the IRS. If the organization changed its name, attach the following documents.

Initial return. Check this box if this is the first time the organization is filing a Form 990 and it hasn’t previously filed a Form 990-EZ, 990-PF, 990-T, or 990-N. Final return/terminated.Check this box if the organization has terminated its existence or ceased to be a § 501(a) or § 527 organization and is filing its final return as an exempt organization or § 4947(a)(1) trust. An organization that checks this box because it has liquidated, terminated, or dissolved during the tax year must also attach Schedule N (Form 990). Schedule NCAUTION! An organization must support any claim to have liquidated, terminated, dissolved, or merged by attaching a certified copy of its articles of dissolution or merger approved by the appropriate state authority. If a certified copy of its articles of dissolution or merger isn’t available, the organization must submit a copy of a resolution or resolutions of its governing body approving plans of liquidation, termination, dissolution, or merger. Application pending. To qualify for tax exemption retroactive to the date of its organization or formation, an organization claiming tax-exempt status under § 501(c) (other than § 501(c)(29)) must generally file an application for recognition of exemption (Form 1023, 1023-EZ, 1024, or 1024-A) within 27 months of the end of the month in which it was legally organized or formed. |

||||||||

| C | Name and address

| Item C. Name and address. Enter the organization’s legal name on the “Name of organization” line. If the organization operates under a name different from its legal name, enter the alternate name on the “Doing Business As” (DBA) line. If multiple DBA names won’t fit on the line, enter one on the line and enter the others on Schedule O (Form 990). If the organization receives its mail in care of a third party (such as an accountant or an attorney), enter on the street address line “C/O” followed by the third party’s name and street address or P.O. box. Include the suite, room, or other unit number after the street address. If the post office doesn’t deliver mail to the street address and the organization has a P.O. box, enter the box number instead of the street address. For foreign addresses, enter the information in the following order: city or town, state or province, the name of the country, and the postal code. Don’t abbreviate the country name. TIP: If a change of address occurs after the return is filed, use Form 8822-B to notify the IRS of the new address. |

||||||||

| D | Employer identification number | Item D. EIN. Each organization (including a subordinate organization of a central organization) must have its own EIN. Use the EIN provided to the organization for filing its Form 990 and federal tax returns. An organization should never use the EIN issued to another organization, even if the organizations are related. The organization must have only one EIN. If it has more than one and hasn’t been advised which to use, notify the: Department of the Treasury State the numbers the organization has, the name and address to which each EIN was assigned, and the address of the organization’s principal office. The IRS will advise the organization which number to use. TIP: A subordinate organization that files a separate Form 990 instead of being included in a group return must use its own EIN, and not that of the central organization. TIP: A § 501(c)(9) voluntary employees’ beneficiary association must use its own EIN and not the EIN of its sponsor. |

||||||||

| E | Telephone number | Item E. Telephone number. Enter a telephone number of the organization that members of the public and government personnel can use during normal business hours to obtain information about the organization’s finances and activities. If the organization doesn’t have a telephone number, enter the telephone number of an organization official who can provide such information. |

||||||||

| F | Name and address of principal officer: | Item F. Name and address of principal officer. The address provided must be a complete mailing address to enable the IRS to communicate with the organization’s current (as of the date this return is filed) principal officer, if necessary. If the officer prefers to be contacted at the organization’s address listed in item C, enter “same as C above.” For purposes of this item, “principal officer” means an officer of the organization who, regardless of title, has ultimate responsibility for implementing the decisions of the organization’s governing body, or for supervising the management, administration, or operation of the organization. TIP: If a change in responsible party occurs after the return is filed, use Form 8822-B to notify the IRS. |

||||||||

| G | Gross receipts $ | Item G. Gross receipts. On Form 990, Part VIII, column A, add line 6b (both columns (i) and (ii)), line 7b (both columns (i) and (ii)), line 8b, line 9b, line 10b, and line 12, and enter the total here. |

||||||||

| H | Group returns.

| Item H. Group returns. If the organization answers “No” to item H(a), it shouldn’t check a box in item H(b). If the organization answers “Yes” to item H(a) but “No” to item H(b), attach a list (not on Schedule O (Form 990)) showing the name, address, and EIN of each local or subordinate organization included in the group return. Additionally, attach a list (not on Schedule O) showing the name, address, and EIN of each subordinate organization not included in the group return. If the organization answers “Yes” to item H(a) and “Yes” to item H(b), attach a list (not on Schedule O) showing the name, address, and EIN of each subordinate organization included in the group return. See Regulations section 1.6033-2(d)(2)(ii). A central organization or subordinate organization filing an individual return should not attach such a list. Enter in item H(c) the four-digit group exemption number (GEN) if the organization is filing a group return, or if the organization is a central or subordinate organization in a group exemption and is filing a separate return. Don’t confuse the four-digit GEN with the nine-digit EIN reported in item D of the form’s heading. A central organization filing a group return must not report its own EIN in item D, but report the special EIN issued for use with the group return. If attaching a list:

|

||||||||

| I | Tax-exempt status.

| Item I. Tax-exempt status. Check the applicable box. If the organization is exempt under § 501(c) (other than § 501(c)(3)), check the second box and insert the appropriate subsection number within the parentheses (for example, “4” for a § 501(c)(4) organization). |

||||||||

| J | Website: | Item J. Website. Enter the organization’s current address for its primary website, as of the date of filing this return. If the organization doesn’t maintain a website, enter “N/A” (not applicable). |

||||||||

| K | Form of organization.

| Item K. Form of organization. Check the box describing the organization’s legal entity form or status under state law in its state of legal domicile. These include corporations, trusts, unincorporated associations, and other entities (for example, partnerships and limited liability companies (LLCs)). |

||||||||

| L | Year of formation: | Item L. Year of formation. Enter the year in which the organization was legally created under state or foreign law. If a corporation, enter the year of incorporation. |

||||||||

| M | State of legal domicile: | Item M. State of legal domicile. For a corporation, enter the state of incorporation (country of incorporation for a foreign corporation formed outside the United States). For a trust or other entity, enter the state whose law governs the organization’s internal affairs (or the foreign country whose law governs for a foreign organization other than a corporation). |

About These Tools

Disclaimer: This website is for informational purposes only and does not constitute professional tax advice.

Source: The content in these tools (such as definitions, questions, and instructions) is from the official IRS Instructions for Form 990, 990-PF, and related schedules and is in the public domain. For the most current official version, please visit https://www.irs.gov/forms-pubs/about-form-990

Special Features & Notes

This is an evolving project, and feedback is always welcome. Please feel free to contact me.

To make the Glossary more user-friendly, the following enhancements have been added:

- User-Added Notes: Italicized text indicates a cross-reference added for clarity and is not part of the official IRS instructions.

- Convenience Links: References to the Internal Revenue Code (IRC) are linked to the Cornell Law School Legal Information Institute (LII) website for the full text.