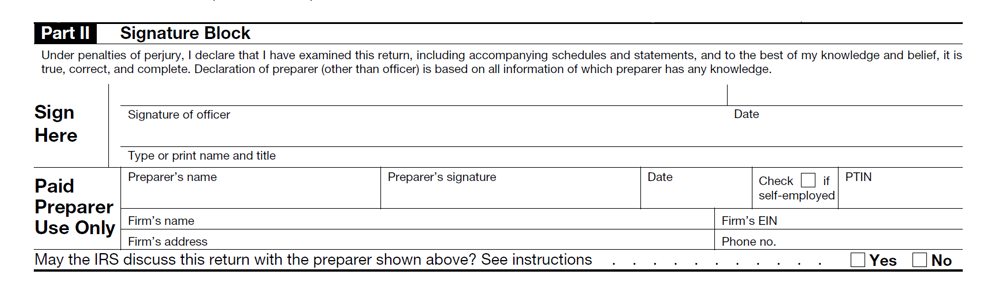

Form 990 Signature Block

Part II

Signature Block

This is a critical part of the return where an officer of the organization signs under penalties of perjury, attesting that the information is true, correct, and complete. This section also includes the signature and information for any paid preparer involved in the return’s preparation.

Sign Here

The return must be signed by the current president, vice president, treasurer, assistant treasurer, chief accounting officer, or other corporate officer (such as a tax officer) who is authorized to sign as of the date this return is filed. A receiver, trustee, or assignee must sign any return he or she files for a corporation or association. See Regulations section 1.6012-3(b)(4). For a trust, the authorized trustee(s) must sign.

The definition of an “officer” for purposes of Part II is different from the definition used to determine which officers to report elsewhere on the form, and from the definition of a principal officer for purposes of the Form 990 heading.

Paid Preparer Use Only

Generally, anyone who is paid to prepare the return must sign the return, list the preparer taxpayer identification number (PTIN), and fill in the other blanks in the Paid Preparer Use Only area. An employee of the filing organization isn’t a paid preparer.

The paid preparer must:

- Sign the return in the space provided for the preparer’s signature;

- Enter the preparer information, including the preparer’s PTIN; and

- Give a copy of the return to the organization.

Any paid preparer can apply for and obtain a PTIN online at IRS.gov/PTIN or by filing Form W-12, IRS Paid Preparer Tax Identification Number (PTIN) Application and Renewal.

CAUTION! Enter the paid preparer’s PTIN, not his or her SSN, in the “PTIN” box in the paid preparer’s block. The IRS won’t redact the paid preparer’s SSN if such SSN is entered on the paid preparer’s block. Because Form 990 is a publicly disclosable document, any information entered in this block will be publicly disclosed (see Appendix D). For more information about applying for a PTIN online, go to IRS.gov/TaxPros.

Note: A paid preparer may sign original or amended returns by rubber stamp, mechanical device, or computer software program.

Paid Preparer Authorization

May the IRS discuss this return with the preparer shown above? ☐Yes ☐No

On the last line of Part II, check “Yes” if the IRS can contact the paid preparer who signed the return to discuss the return. This authorization applies only to the individual whose signature appears in the Paid Preparer Use Only section of Form 990. It doesn’t apply to the firm, if any, shown in that section.

By checking “Yes,” the organization is authorizing the IRS to contact the paid preparer to answer any questions that arise during the processing of the return. The organization is also authorizing the paid preparer to:

- Give the IRS any information missing from the return;

- Call the IRS for information about processing the return; and

- Respond to certain IRS notices about math errors, offsets, and return preparation.

The organization isn’t authorizing the paid preparer to bind the organization to anything or otherwise represent the organization before the IRS.

The authorization will automatically end no later than the due date (excluding extensions) for filing of the organization’s subsequent year’s Form 990. If the organization wants to expand the paid preparer’s authorization or revoke it before it ends, see Pub. 947, Practice Before the IRS and Power of Attorney.

Check “No” if the IRS should contact the organization or its principal officer listed in item F of the heading on page 1, rather than the paid preparer.

About These Tools

Disclaimer: This website is for informational purposes only and does not constitute professional tax advice.

Source: The content in these tools (such as definitions, questions, and instructions) is from the official IRS Instructions for Form 990, 990-PF, and related schedules and is in the public domain. For the most current official version, please visit https://www.irs.gov/forms-pubs/about-form-990

Special Features & Notes

This is an evolving project, and feedback is always welcome. Please feel free to contact me.

To make the Glossary more user-friendly, the following enhancements have been added:

- User-Added Notes: Italicized text indicates a cross-reference added for clarity and is not part of the official IRS instructions.

- Convenience Links: References to the Internal Revenue Code (IRC) are linked to the Cornell Law School Legal Information Institute (LII) website for the full text.